|

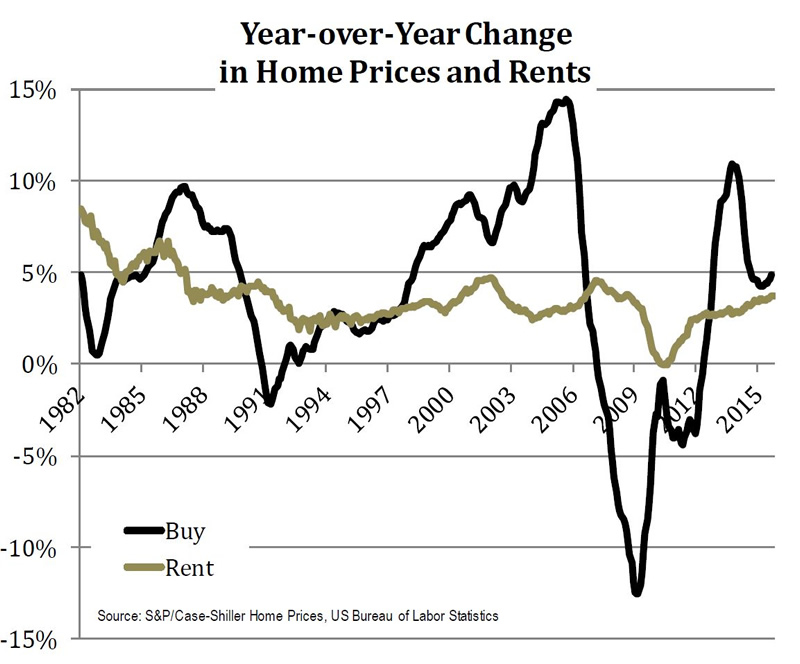

S&P/Case Shiller Reports Home Prices Up 4.9% in September Year-Over-Year New York, November 24, 2015 – S&P Dow Jones Indices today released the latest results for the S&P/Case-Shiller Home Price Indices, the leading measure of U.S. home prices. Data released today for September 2015 show that home prices continued their rise across the country over the last 12 months. More than 27 years of history for these data series is available, and can be accessed in full by going to www.homeprice.spdji.com. Additional content on the housing market can also be found on S&P Dow Jones Indices’ housing blog: www.housingviews.com. Year-over-Year San Francisco, Denver and Portland reported the highest year-over-year gains among the 20 cities with double-digit price increases of 11.2%, 10.9%, and 10.1%, respectively. Seventeen cities reported greater price increases in the year ending September 2015 versus the year ending August 2015. Phoenix had the longest streak of year-over-year increases, reporting a gain of 5.3% in September 2015, the tenth consecutive increase in annual price gains. Month-over-Month Analysis “The strength seen in home prices since the bottom in 2012 led some to wonder if we’re entering a new bubble. While bubbles can only be reliably identified in hindsight, one useful measure compares the increase in home prices to the change in rents. The first chart below shows the year-over-year change in the S&P/Case-Shiller National Home Price Index and the year-over-year change in the rent of primary residence series reported as part of the Consumer Price Index. Home prices are far more volatile. At the same time, the most recent data do not show a huge spread between the two series.” “Another question raised by consistent real (or inflation adjusted) home price increases is whether the prices are squeezing people out of the market. One measure of affordability is based on median income, median home price, and mortgage rate; a value of 100 on the chart below indicates a home buyer at the median income can afford the median price home. As shown on the chart, affordability is more than adequate for a median income buyer now but has slipped a bit recently.”

|

| © 2006 - 2022. All Rights Reserved. |