|

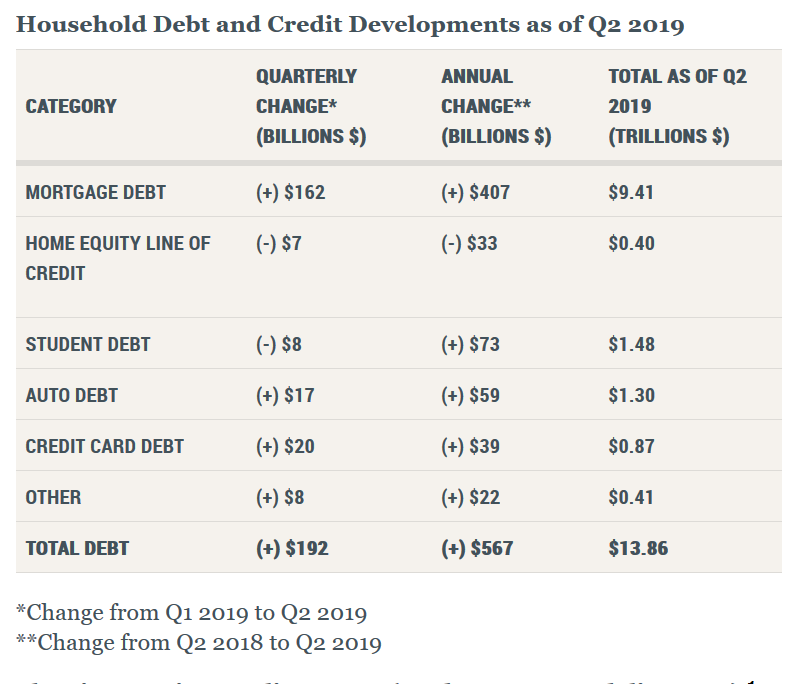

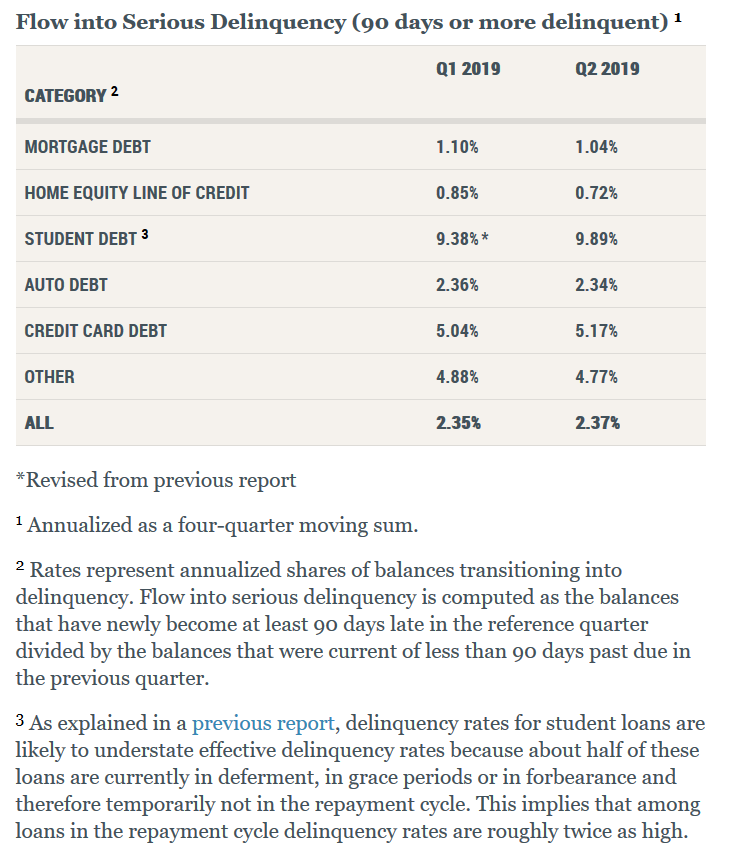

Total Household Debt Climbs for 20th Straight Quarter as Mortgage Debt and Originations Rise NEW YORK – The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit, which shows that total household debt increased by $192 billion (1.4%) to $13.86 trillion in the second quarter of 2019. It was the 20th consecutive quarter with an increase, and the total is now $1.2 trillion higher, in nominal terms, than the previous peak of $12.68 trillion in the third quarter of 2008. The Report is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample of individual- and household-level debt and credit records drawn from anonymized Equifax credit data. Mortgage balances—the largest component of household debt—rose by $162 billion in the second quarter to $9.4 trillion, surpassing the high of $9.3 trillion in the third quarter of 2008. Mortgage originations, which include mortgage refinances, also increased by $130 billion to $474 billion, the highest volume seen since the third quarter of 2017. Meanwhile, the share of credit card balances transitioning into 90+ day delinquency rose to 5.2% from 5.0% last quarter, at an annual rate, continuing an upward trend that began in 2017. “While nominal mortgage balances are now slightly above the previous peak seen in the third quarter of 2008, mortgage delinquencies and the average credit profile of mortgage borrowers have continued to improve,” said Wilbert van der Klaauw, senior vice president at the New York Fed. “The data suggest a more nuanced picture for other forms of household debt, with credit card delinquency rates continuing to rise.” The New York Fed also issued an accompanying blog post that takes a deeper dive into the measurement of, and recent changes in, delinquency rates by loan type. The Report includes a one-page summary of key takeaways and their supporting data points. Overarching trends from the Report’s summary include: Housing Debt

Non-Housing Debt

Bankruptcy Notations, Collection Accounts, and Credit Inquiries

|

| © 2006 - 2022. All Rights Reserved. |